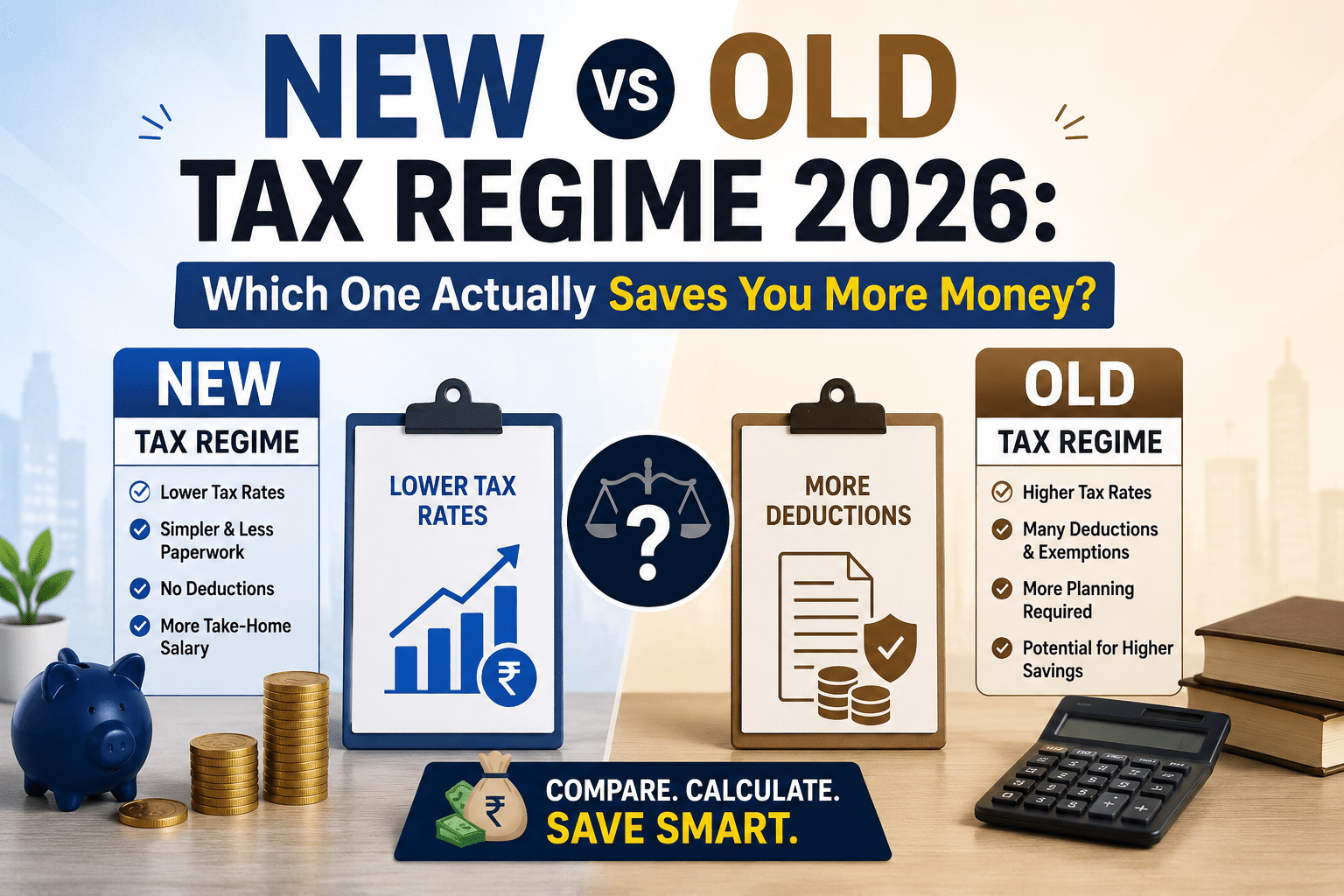

Every year during ITR season, the same question echoes across offices, WhatsApp groups, and finance forums: “Should I go with the new tax regime or stick with the old one?”

The answer is not the same for everyone. It depends on your salary, your investments, your rent situation, and your home loan. This guide breaks it down clearly so you can make the right call before the July 31 deadline.

The Core Difference in One Line

The new regime gives you lower tax rates but almost no deductions. The old regime gives you higher rates but lets you reduce your taxable income significantly through exemptions and deductions.

Tax Slabs: New Regime vs Old Regime (FY 2025-26)

New Tax Regime Slabs (Default for all taxpayers)

| Income Slab | Tax Rate |

| Up to ₹4 lakh | Nil |

| ₹4 lakh – ₹8 lakh | 5% |

| ₹8 lakh – ₹12 lakh | 10% |

| ₹12 lakh – ₹16 lakh | 15% |

| ₹16 lakh – ₹20 lakh | 20% |

| ₹20 lakh – ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

Key benefit: Tax rebate under Section 87A makes income up to ₹12 lakh completely tax-free under the new regime. A standard deduction of ₹75,000 is also available.

Old Tax Regime Slabs (Below 60 years)

| Income Slab | Tax Rate |

| Up to ₹2.5 lakh | Nil |

| ₹2.5 lakh – ₹5 lakh | 5% |

| ₹5 lakh – ₹10 lakh | 20% |

| Above ₹10 lakh | 30% |

Key benefit: All major deductions are available — 80C (₹1.5 lakh), HRA, 80D, home loan interest (₹2 lakh), and more.

What Deductions Can You Claim?

| Deduction | Old Regime | New Regime |

| Standard deduction | ₹50,000 | ₹75,000 |

| Section 80C (PPF, ELSS, LIC) | ✅ Up to ₹1.5 lakh | ❌ Not allowed |

| Section 80D (Health insurance) | ✅ Up to ₹25,000 | ❌ Not allowed |

| HRA exemption | ✅ Allowed | ❌ Not allowed |

| Home loan interest (self-occupied) | ✅ Up to ₹2 lakh | ❌ Not allowed |

| NPS employer contribution (80CCD(2)) | ✅ Up to 14% of salary | ✅ Allowed |

| Home loan interest (let-out property) | ✅ No limit | ✅ Allowed |

Who Should Choose the New Tax Regime?

The new regime works better for you if:

- Your gross income is up to ₹12 lakh (zero tax after rebate + standard deduction)

- You have minimal investments in 80C instruments

- You do not pay rent or have HRA

- You have no home loan on a self-occupied property

- You prefer simplicity over tax planning

Who Should Choose the Old Tax Regime?

The old regime works better for you if:

- You pay rent in a metro city (HRA exemption is significant)

- You have a home loan with interest above ₹1.5 lakh per year

- You invest the full ₹1.5 lakh under Section 80C

- You pay health insurance premiums for yourself and parents

- Your income is above ₹15–20 lakh and deductions are substantial

Real-World Example: Which Regime Wins?

Scenario: Salaried employee, ₹15 lakh CTC, metro city, home loan + 80C investments

| Component | Old Regime | New Regime |

| Gross salary | ₹15,00,000 | ₹15,00,000 |

| Standard deduction | −₹50,000 | −₹75,000 |

| HRA exemption | −₹1,20,000 | ❌ |

| 80C investments | −₹1,50,000 | ❌ |

| Home loan interest | −₹2,00,000 | ❌ |

| 80D (health insurance) | −₹25,000 | ❌ |

| Taxable income | ₹9,55,000 | ₹14,25,000 |

| Tax payable | ~₹1,17,000 | ~₹1,57,500 |

In this case, the old regime saves approximately ₹40,000.

However, for the same person with no HRA, no home loan, and minimal 80C:

| Component | Old Regime | New Regime |

| Gross salary | ₹15,00,000 | ₹15,00,000 |

| Standard deduction | −₹50,000 | −₹75,000 |

| Taxable income | ₹14,50,000 | ₹14,25,000 |

| Tax payable | ~₹2,32,500 | ~₹1,57,500 |

Here the new regime saves ₹75,000.

The Switch Rule: Can You Change Every Year?

- Salaried employees: Yes. You can switch between regimes every year when filing your ITR.

- Business owners / freelancers: You can switch only once from new to old, and switch back only once.

Important: If you miss the July 31 deadline and file a belated return, you cannot opt for the old regime — you are automatically placed in the new regime.

Frequently Asked Questions

Q: Is the new regime mandatory from FY 2025-26?

It is now the default regime, but it is not mandatory. You can actively opt for the old regime when filing your ITR.

Q: Can I claim 80C if I choose the new regime?

No. Section 80C deductions are not available under the new tax regime.

Q: What is the break-even point between the two regimes?

Generally, if your eligible deductions exceed ₹3.75 lakh (for income around ₹15 lakh), the old regime is better. Below that threshold, the new regime usually wins.

Q: My employer deducted TDS under one regime. Can I change at filing time?

Yes. You can always switch when filing your ITR, regardless of which regime your employer used for TDS.