Every few years, there’s talk about “major tax reforms.” Most people ignore it until March arrives and their CA asks for documents.

But the proposed Income Tax Rules 2026 in India seem slightly different. This time, the focus is not just on changing slabs. It’s more about cleaning up the system — making it tighter, more digital, and harder to manipulate.

If you earn a salary, run a business, or invest regularly, these changes are worth understanding properly.

Why Is India Even Changing the Income Tax Rules Again?

To be honest, the government has been trying to simplify the tax system for years.

First came digitization.

Then AIS reporting.

Then the new tax regime.

Now, the 2026 proposals appear to push things further in one direction:

👉 fewer exemptions, more transparency, and stronger tracking of financial transactions.

From the government’s point of view, the goals are simple:

- Reduce disputes

- Increase compliance

- Make filing easier

- Prevent tax leakage

Whether that actually makes life easier for taxpayers depends on how these rules are implemented.

A Quick Look Back – How Tax Reforms Have Evolved

If you think about it, income tax in India used to be much more complicated.

There were multiple deductions, complicated paperwork, and manual scrutiny. Over time, the system became digital. Now, almost everything reflects automatically in your AIS.

The new tax regime introduced a few years ago was another attempt to simplify things: lower tax rates, but fewer deductions.

The 2026 changes look like a continuation of that thinking.

So What May Actually Change in 2026?

Let’s talk practically.

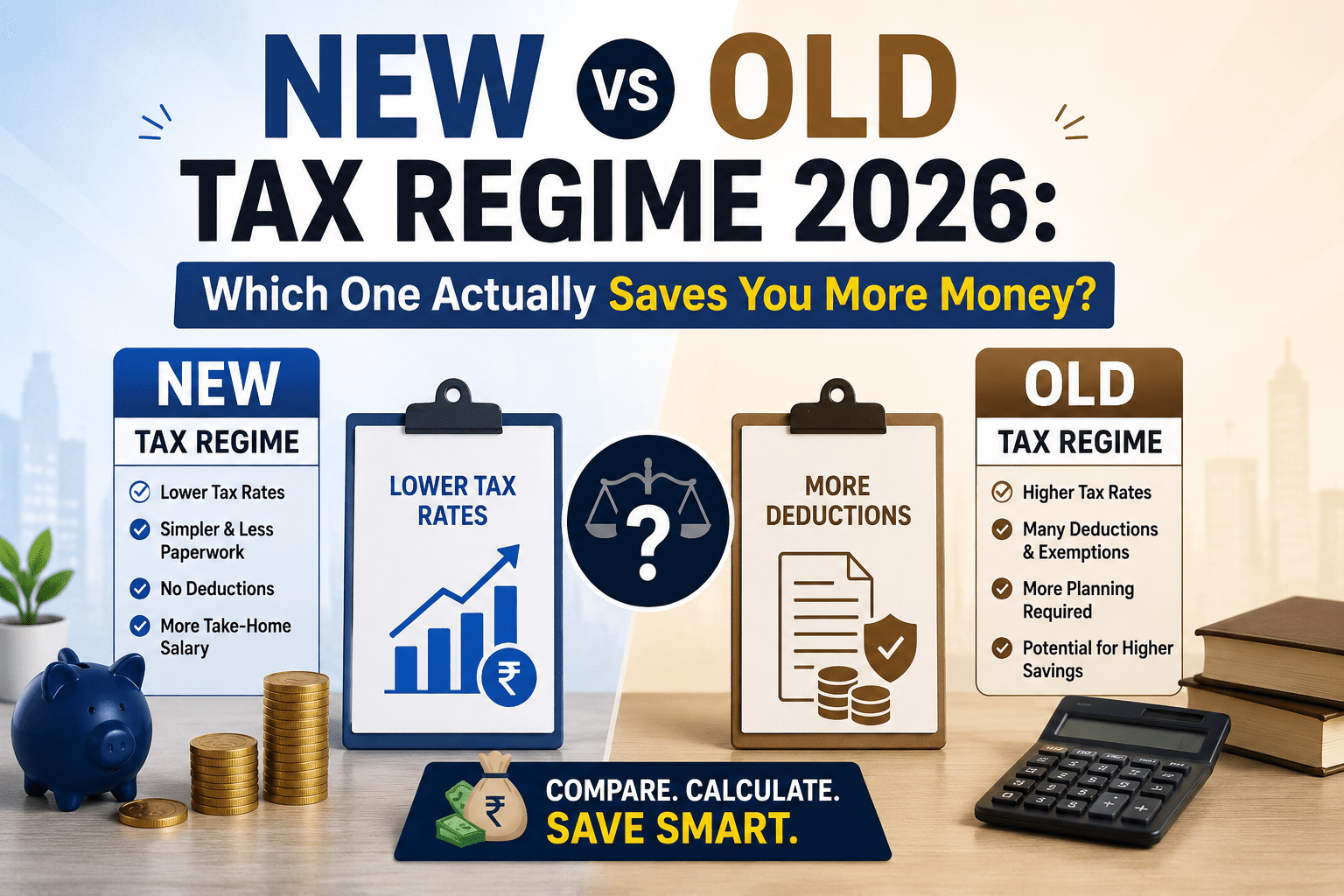

1. Old vs New Tax Regime

This debate isn’t going away.

Under the old regime, people claim:

- HRA

- 80C investments

- Home loan interest

- Medical insurance

Under the new regime, you get:

- Lower tax rates

- Fewer deductions

- Simpler structure

The government seems to be encouraging the new regime more aggressively. Over time, exemptions under the old regime may gradually reduce.

For salaried individuals with fewer investments, the new regime may make sense. For those claiming high deductions, the old regime might still work better.

There is no one-size-fits-all answer.

2. HRA and Allowances

HRA misuse has been a common issue. Many people claim rent exemptions casually without proper documentation.

The proposed rules suggest tighter checks. Expect stricter verification and better digital cross-checking of landlord PAN details.

If you claim HRA, keep documentation clean.

3. PAN and Aadhaar Linkage

At this point, PAN-Aadhaar linkage is not optional.

Under the proposed structure, financial systems are increasingly interconnected. If your PAN is inactive or not properly linked, you may face restrictions in banking, investments, or filing.

This is more of a compliance clean-up move.

4. Gift and Voucher Taxation

Gifts above a certain threshold are already taxable. But digital tracking makes it easier for authorities to see high-value transactions.

Corporate gift vouchers, transfers, or unusual credits in bank accounts may attract attention if not properly disclosed.

Again, transparency is the theme.

5. TDS and Business Compliance

For business owners, the bigger change is stricter reconciliation.

Turnover in GST must match income tax reporting.

TDS deductions must reflect correctly.

AIS data must be reconciled before filing.

Mismatch is where notices usually begin.

Businesses that maintain clean books won’t struggle. Those relying on informal adjustments may find it harder now.

Who Feels the Impact the Most?

Salaried Employees

If your income is straightforward and documented, you won’t feel dramatic change. The main decision remains choosing the right regime.

But if you claim multiple exemptions, documentation becomes more important.

Business Owners

Compliance pressure is higher. Digital tracking leaves less room for casual errors.

Accounting discipline matters more now than ever.

Investors

Capital gains are being monitored closely through broker reporting systems.

If you trade frequently or invest across platforms, you must reconcile before filing. Ignoring AIS is risky.

Is This Good or Bad?

It depends on perspective.

For honest taxpayers with clean documentation, simplification can actually reduce confusion.

For those who relied heavily on grey areas or aggressive deductions, the system may feel stricter.

Overall, the direction seems clear:

👉 Simpler structure.

👉 Fewer exemptions.

👉 Stronger digital oversight.

What Should You Do Now?

Instead of waiting until the end of the financial year:

- Compare tax regimes early

- Organize investment documents

- Avoid last-minute tax-saving decisions

- Keep accounting records updated

- Reconcile AIS before filing

Tax planning is no longer about saving maximum tax at the last minute. It’s about staying aligned with a system that is becoming increasingly automated.

Final Thoughts

The New Income Tax Rules 2026 in India are not about shocking tax hikes. They appear to be about tightening the system and pushing long-term simplification.

For most people, the real impact will depend on income type and compliance habits.

If your documentation is clear and your reporting is accurate, these changes won’t feel dramatic.

But if your tax planning is reactive and disorganized, 2026 may feel uncomfortable.

Planning early is no longer optional — it’s practical.